Are you concerned about being smart with your taxes? Tax planning ahead of time can save you a lot of headaches and money in the long run.

Tax planning doesn’t have to be as complicated as you think it is. It is a well-defined process ideally done throughout the year, that helps you save your hard-earned money.

You cannot avoid filing taxes every year, but that doesn’t mean you also avoid the choice to save money when filing your taxes.

We are not asking you to spend your weekends over this either. All you need to spend is some quality time consistently every month. What do you do? You review your current investments and expenses and check where you can move them to make them tax-friendly.

You are not in this alone. You can take help of financial experts like Vittae, that will guide you every step of the way.

Let’s demystify tax planning and also understand why it is important, and how we can help you!

What is Tax Planning?

Tax planning refers to the process of analyzing the financial status of an entity or individual to increase tax savings.

The main purpose of tax planning is to build tax efficiency. This means you have to ensure that all the elements of your financial plan are in line. This helps in an overall reduction of your tax burden and increases your tax deductions.

Tax planning is not a one-time action! It continues throughout the year so that you make the most of it by the end of the financial year.

You must file taxes and returns during the assessment period after March 31st. However, you must make tax planning decisions across the financial year.

If you are still wondering if you really need tax planning, let’s dig a little deeper.

Why is tax planning important?

Minimizing tax liability

Tax planning helps individuals and businesses legally minimize the tax amount they owe. This is done by taking advantage of available tax deductions, credits, and exemptions.

Maximizing cash flow

When taxes are minimized, the funds saved can be used for other purposes. Such as investing, saving, or paying off debt, which can help increase cash flow.

Avoiding penalties and interest

Proper tax planning can help taxpayers avoid penalties and interest for underpayment or late payment of taxes.

Risk mitigation

Tax laws and regulations can be complex and constantly changing. Tax planning can help reduce the risk of non-compliance with tax laws and regulations. This saves you from paying hefty penalties or dealing with legal issues.

Planning for the future

Tax planning can help individuals and businesses plan for the future. By considering the tax implications of future actions and decisions, you are not only saving money but also securing your future.

Benefits of Tax Planning

Reduction of tax liability

Tax planning helps individuals and businesses to legally reduce their tax liability, which can increase their take-home income or profits. This is a given that most folks fail to see. You often see all the forms and paperwork and forget how in the long term, the benefit is yours.

Improved cash flow

By reducing tax liability, tax planning can help individuals and businesses to free up cash. As the logic goes, this cash can be used for other purposes such as investment, saving, or debt repayment.

Better financial management

Proper tax planning can help individuals and businesses to better manage finances. This is done by forecasting your tax liability and designing a tax-efficient strategy. The aim of this strategy is to minimize the impact of taxes on your personal or business finances.

Avoidance of penalties and interest

When you plan ahead, as a taxpayer you can avoid or minimize penalties. You won’t have to pay interest for underpayment, late payment, or non-compliance with tax laws and regulations.

Better business decisions

Tax planning can help businesses to make better decisions by considering the tax implications of potential business transactions or investment opportunities. This allows you to make informed decisions that align with their overall financial goals.

Tax Saving Instruments

The following instruments and expenses will help you increase your tax savings.

House Rent Allowance

A salaried individual having rented accommodation can get the benefit of HRA (House Rent Allowance). This could be totally or partially exempted from income tax.

Leave Travel

Domestic travel can be claimed as LTA. Only travel costs can be claimed. The modes of such travel must be either railway, air travel, or public transport.

LTA can be claimed twice in a block of four years. In case an individual doesn’t use this exemption within a block, he/she could carry the same to the next block.

Children’s Education & Hostel Allowance

Children’s Educational Allowance: An allowance of ₹100 per month is allowed per child for up to two children studying in an educational institution.

Hostel Expenditure Allowance: An allowance of ₹ 300 per month per child for up to two children is given to those staying in hostels.

Telephone & Broadband allowance

The income tax law allows an employee to claim a tax-free reimbursement of expenses incurred.

If you are an employee, you can claim reimbursement of the actual bill amount paid or the amount provided in the salary package, whichever is lower.

Car Maintenance Allowance

Maintenance and fuel expenses are reimbursed by the employer. If the employee owns the car (used for official and personal use), an exemption of

₹ 1,800 per month ( + 900 per month if the driver is provided)

(for cars with engine capacity up to 1,600 cc)

or

₹ 2,400 per month ( + 900 per month if the driver is provided)

(for cars with engine capacity of more than 1,600 cc)

Housing Loan

Interest on House Loan repayment can be claimed up to ₹ 200,000 under Section 24(b).

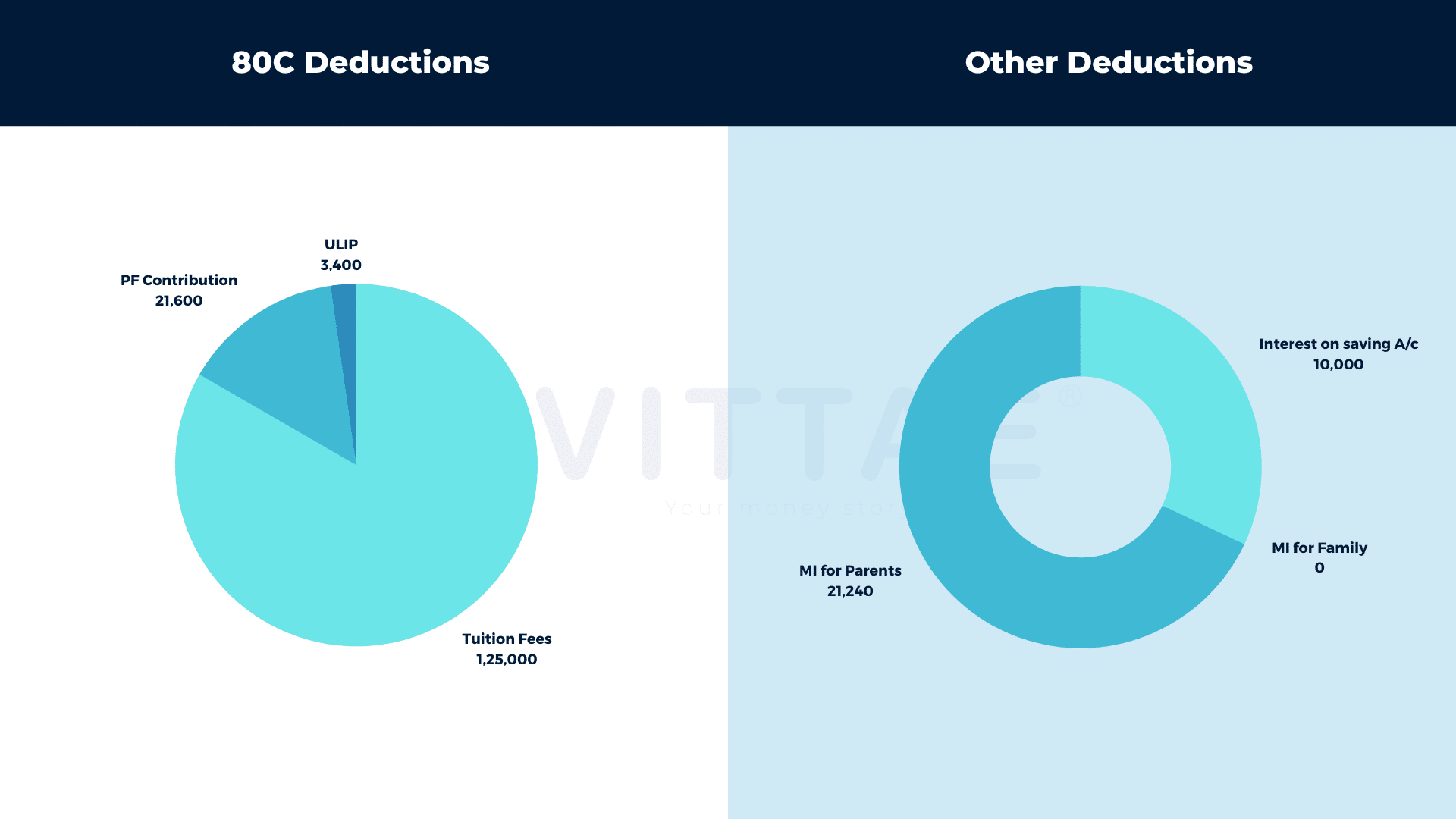

Investments under Section 80C

Public Provident Fund, Employee Provident Fund, Voluntary Provident Fund, Five-Year Post Office Time Deposit, and ELSS (Equity Linked Savings Scheme) are some of the investments that will save you money under Section 80C.

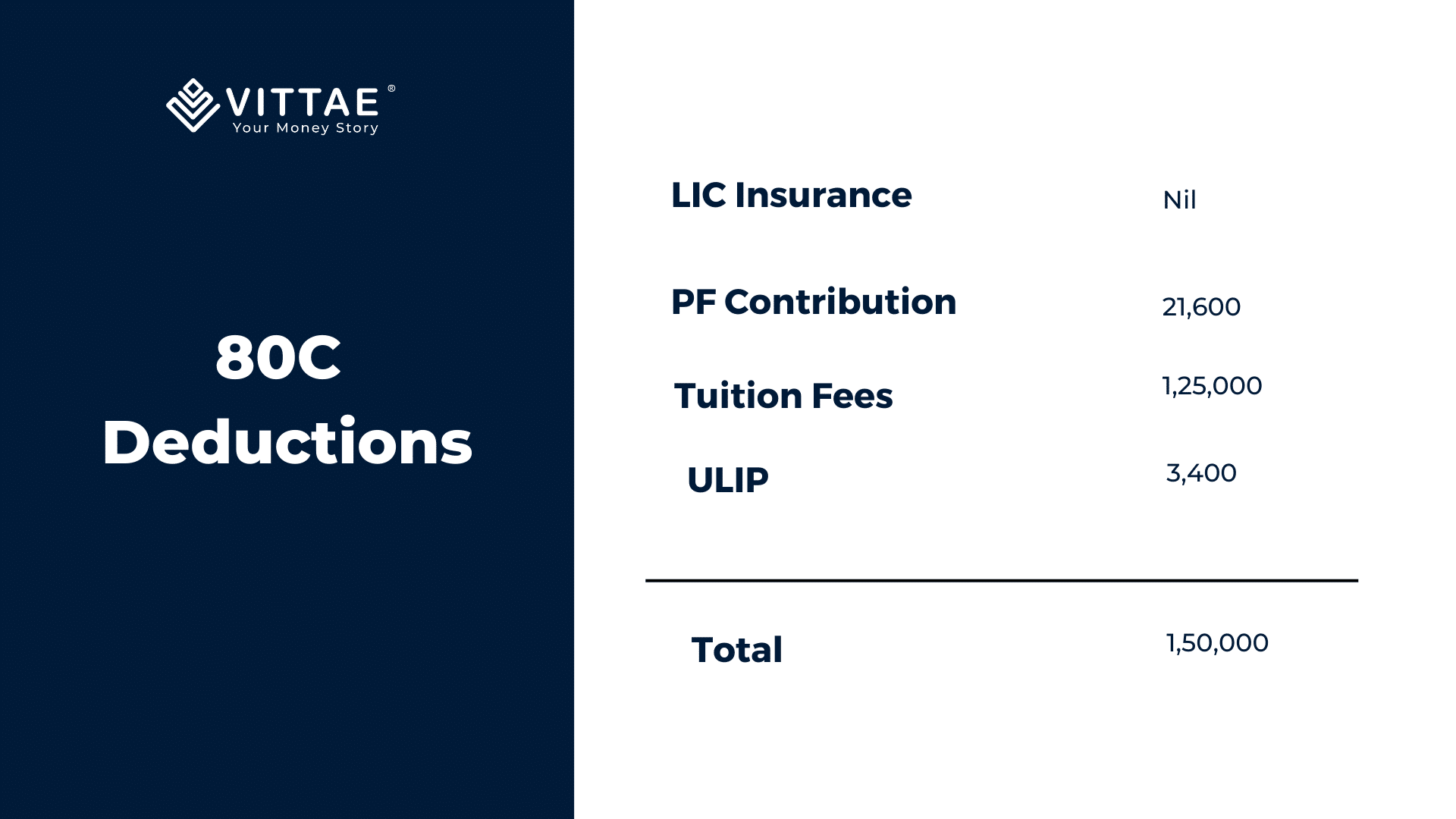

80C Tax Deductions

The following expenses qualify for tax deduction under 80C:

- Life Insurance Policy premium payments

- Children’s tuition fees

- Repayment of principal amount on home loan

Medical Insurance 80 D

Section 80D of the Income Tax Act permits deductions on the amount spent by an individual towards the premium of a health insurance policy.

This includes payment made on behalf of a spouse, children, parents, or self to a Central Government Notified health plan.

Donation 80 G

Section 80G encourages taxpayers to donate to funds and charitable institutions, offering tax benefits on monetary donations. All assesses are eligible for this deduction, subject to them providing proof of payment.

Steps To Follow When Doing Tax Planning:

Evaluate your tax situation

Take a closer look at your income streams, sources of income, and taxable income to determine how much tax you owe.

Identify tax deductions and credits

Determine what deductions and credits you qualify for, such as charitable contributions, mortgage interest, property taxes, and education expenses. Check how they can impact your tax liability.

Consider retirement account

Saving for retirement in a tax-advantaged account can also reduce your taxable income and help you plan for your financial future.

Plan for itemized deductions

Determine if the total amount of itemized deductions will exceed the standard deduction by calculating and comparing both. Make strategic moves to maximize your deductions.

Keep track of receipts and expenses

Keep accurate records of your expenses, receipts, and documents. Doing this can support your deductions and credit claims (in the case of an audit).

Consult a tax professional

A tax professional can help you navigate the tax code, maximize your tax savings, and identify opportunities for tax planning that you might have missed on your own.

At Vittae, we’ll file your taxes for free. Not just that, we’ll help you with a detailed Tax Report that guides you on your tax planning strategies.

Review and adjust your tax plan

Make sure to review your tax plan annually. This will reflect changes in your income, expenses, tax laws, and regulations. You must further adjust it accordingly to ensure your tax plan is aligned with your financial goals.

Tax Planning vs. Tax Filing

Tax planning is strategizing and optimizing your financial affairs to minimize your tax liability.

In contrast, tax filing involves completing and submitting your tax returns. This includes reporting your income, expenses, credits, and deductions, paying your taxes, or asking for a refund.

Below are various factors that differentiate tax planning from tax filing:

Timing

Tax planning typically occurs throughout the year, as taxpayers aim to take advantage of tax benefits and avoid overpaying taxes. In contrast, tax filing occurs annually.

Goal

The goal of tax planning is to minimize tax liability while planning for financial goals or achieving a favorable tax position.

Tax filing aims to comply with tax laws and regulations and accurately report your income, expenses, credits, and deductions.

Complexity

Tax planning is often more complex than tax filing. It involves designing and implementing strategies that consider your entire financial situation.

Tax filing, on the other hand, is often a straightforward task of filling out tax forms and submitting them with accuracy.

Professional assistance

Tax planning may require the expertise of tax professionals such as accountants, financial planners, or tax attorneys to evaluate the options and execute the strategies.

Tax filing can be done without professional help, although it is often advisable to seek assistance if you have a complicated tax situation.

In Conclusion

Every financial plan is better when you include tax planning. It helps optimize your tax liability within the framework of legal regulations. It is important that you make tax planning an essential aspect of your financial plan as well.

Effective tax planning can minimize the tax burden and maximize deductions. This ultimately leads to significant savings and improved financial stability.

By staying up-to-date with tax laws and regulations you can avoid penalties and other legal consequences of non-compliance.

For example, if you invest in certain tax-saving financial instruments such as Public Provident Fund (PPF), National Pension System (NPS), or Equity-Linked Savings Scheme (ELSS), you can claim deductions from your taxable income.

If you are a business owner, you can claim deductions for expenses. Such as salaries, rent, and depreciation. This can reduce your taxable income and lower your overall tax liability.

In simple words, tax planning is important and unavoidable. It can help you keep more of your hard-earned money in your pocket.