At the end of every month, are you relaxed with no worry or are you anxiously waiting for next month’s salary to be credited? Is a “reasonable” purchase in the first week now seeming like an “expensive” indulgence in the last week of the month?

If you’ve answered yes to either of these questions, it’s a sign that you need help with expense tracking and money management.

Have you noticed that when planning for finances, most of us start with saving more and don’t pay attention to spending less? We tend to focus on how to earn a six-figure income but avoid checking the four-figure monthly expenses.

It’s common to know how much monthly EMI is getting debited. The question is, do you have an account of the money spent on chai/coffee every month?

We all know following a budget and tracking your expenses is a good practice, but not many of us actively do it. It’s like when a person looking for their phone, searches for it everywhere else but in their pocket (where they actually left it).

Let’s understand the importance of budgeting, how to make a budget, the benefits of expense tracking, and how easy it is to apply these in your daily life.

What is Budgeting?

Remember how your parents gave you pocket money when you were a kid? You would immediately get to planning how to spend it, or save up for something big.

A budget is the same plan you made then, only on a larger scale.

From wanting the biggest toy in the store to saving up for the latest phone in the market, not much has changed. However, how we perceive savings and budgeting has evolved over time.

Budgeting is creating a spending plan to help you understand how much money you can save, spend and also invest.

This simple process helps you immensely to prioritize your spending and increase your savings.

How to make a Personal Budget?

Let’s see how you can design your Personal Budget in four simple steps.

Check your account statements

No matter how small or big a task, you always start at the basics. This step includes two fundamental actions.

- First, check your account balance.

- Next, check your account statements.

An account statement is a summary of all your fixed and recurring expenses. For example, a fixed expense is a purchase of a new bike, whereas a recurring expense would be the monthly servicing/maintenance charges spent on it.

Keep a note of how much you’re spending on both types of expenses.

Categorize your expenses

Each of you leads a different lifestyle with varying expenses. Categorize your recurring expenses into three or more types.

A few common expenses to include in your budget are

- Housing Expenses (Rent/Loan payment)

- Groceries & essential items

- Vehicle/Transportation costs

- Internet & Cable

- Entertainment & recreation

- Healthcare (Insurance payment)

Don’t forget to count your “impulse buys” that are a bit heavy on the pocket.

An impulse buy is an unplanned spending decision that occurs seconds before you buy the product/service.

In simple words, it is a spur-of-the-moment purchase.

For example, when waiting for billing at a supermarket counter, you tend to add chocolates/gum impulsively. They were most probably not on your grocery list, but you buy them anyway.

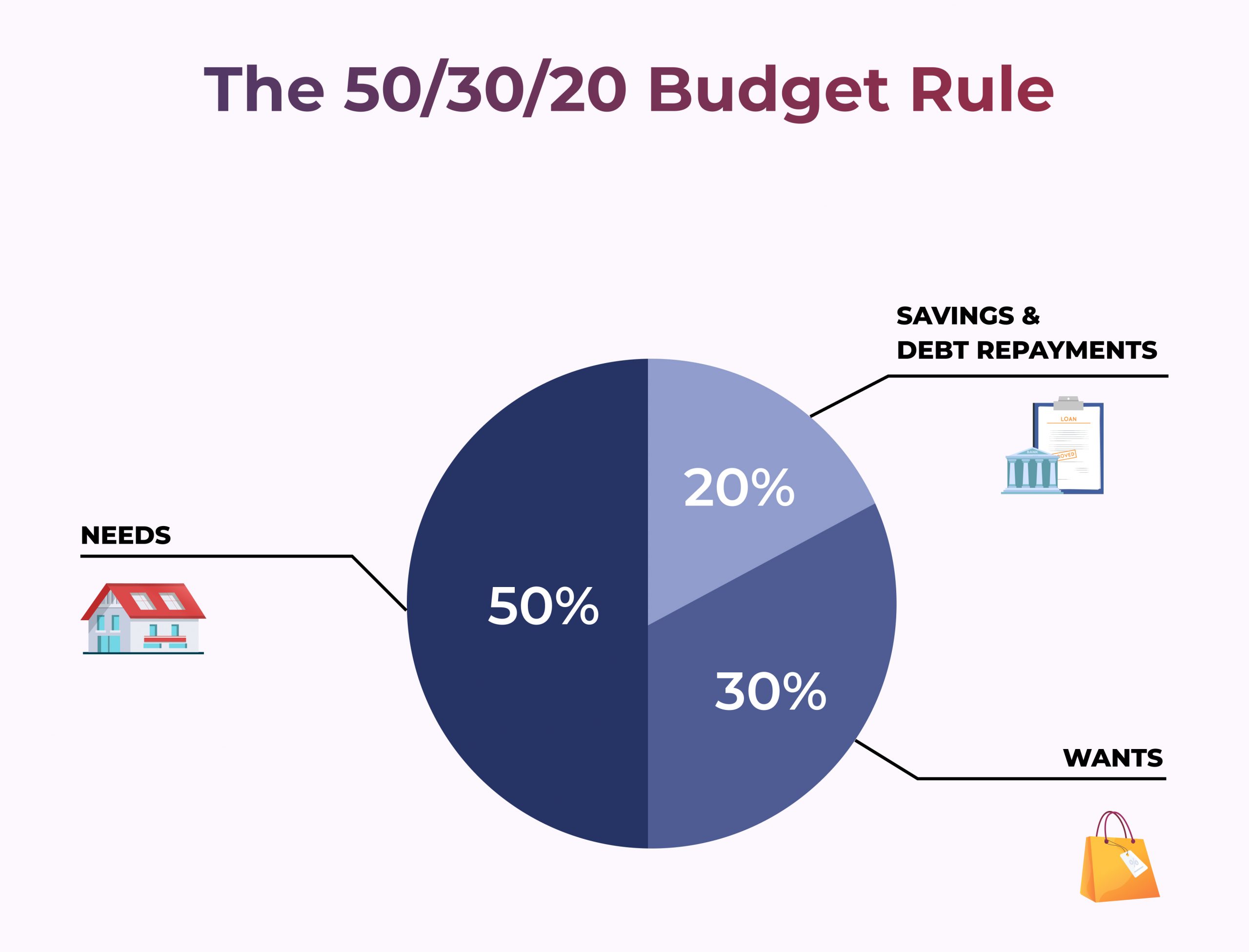

Apply the 50/30/20 budgeting rule

The 50/30/20 rule is an old yet practical rule. This method will help you manage your money in a smart and sustainable manner.

Follow this basic rule to divide your monthly income (after-tax) into three sections.

50% for needs

Needs are the basic expenses that are necessary for survival such as rent, groceries, and education expenses.

30% for wants

Wants are not crucial for survival, but are expenses that often bring joy such as dining out, shopping, and travelling.

20% for savings/paying off debt

Savings is the money you save for future needs such as emergency fund and insurance. Savings can also include the amount to pay off debt such as loan EMIs.

Allocating the mentioned percentages of monthly income to needs, wants and savings helps you manage your money effectively. Dividing your income in this format helps you compare to what you should ideally do versus what you are currently doing.

Organize, Prioritize & Cut

Our parents constantly reminded us not to spend our pocket money all at once. Similarly, you’ve also got to stick to your budget to save more and spend less. This step determines how well you budget your money.

Organize – all your expenses into needs and wants.

Prioritize – your needs over wants (this is a deciding factor to decrease your spending)

Cut – your expenses by setting limits to each want (like shopping)

After you’ve made the budget using these 4 steps, you now come to Expense Tracking.

What is Expense Tracking?

If you’ve figured out your monthly budget, then Expense Tracking is a piece of cake. It’s literally a track of the money that goes out of your pocket and of the time it went out.

Example: Spent ₹500 buying Pizza on 15th March 2023.

Expense Tracking is a simple tool to check the inflow and outflow of money from your account. That’s why it is important to create a detailed personal budget. Your personal budget becomes a guide that you’ll refer to while tracking expenses. Checking it from time to time will ensure you don’t cross your spending limits.

Why is Expense Tracking Important?

Every month, you have recurring expenses from rent and groceries to unforeseen expenses like shopping. Have you ever wondered why you are never able to pinpoint exactly how much you have spent by the end of the month?

We agree you might have a rough estimate of the amount. That’s precisely our point. Most of us always seem to have only an estimated figure to calculate our spending.

For example, you spend ₹3000 per month (₹750 per week) on groceries. Let’s assume in reality you’re spending ₹5000 (₹1250 per week) per month.

That means you’re assuming you are spending only ₹36,000 a year, while in reality, your grocery expenses for an entire year are ₹60,000.

When you were thinking “oh! I spent just ₹2000 more this month”,

turns out to be “This year, I spent ₹24,000 extra!!”

This example is not to discuss inflation or the increasing rates of groceries. It’s to emphasize that because you don’t track expenses, you are losing out on savings and potential investment opportunities.

How to track your expenses?

Use an expense tracker app

The old-school way was to write every daily expense in a book. In today’s day and age of technological advancement, expense tracking doesn’t require paper and a pen. A lot of folks also make an Excel spreadsheet of their monthly and annual budget.

Worry not, all you have to do is tap on your phone screen and viola, it’s done!

There are multiple expense tracking apps in the market that allow you to update your daily/weekly/monthly expenses with just a few clicks on a screen. All you have to do is enter your details, select your expense categories, and start tracking!

Use UPI for transactions

At times, updating about every spending throughout the day (at the time you spend it) seems inconvenient. Use your UPI apps to make the transactions, so you can refer to your expenses later.

Don’t forget to mention what the expense category is in the UPI app, at the time of making the payment.

Expense Tracking tips to keep you ‘on track’

Start with a weekly budget

There are two possibilities when you start with a monthly budget.

- First, you keep extensive track of every small expense to save big.

- Second, you don’t stick to tracking every expense because you assumed you have 30 days to make up for it.

We suggest taking an extra five minutes, after making the monthly budget to create a weekly budget. It’s quicker to check and easier to track.

Stick to the budget

If you’ve organized your wants and needs, and are aware of your spending limits, stick to them. Are you thinking “it’s easier said than done”?

We’re sure you’ve set these limits after a thorough analysis, to prioritize your needs over wants. Remind yourself of those reasons and stay on track.

Develop good money habits

Let’s say you’re at a mall with a friend, and you realize you’ve already crossed your weekly budget for shopping. This doesn’t give you permission to borrow from your friend to buy new jeans.

While tracking your expenses, ensure you don’t increase your debt. Remind yourself of the 50/30/20 budgeting rule.

In conclusion

Simplify your money management with simple practices such as regular budgeting and daily expense tracking. These are the first steps that lead to financial stability. Being consistent and building financial discipline are key takeaways from these practices.

We are confident, that in a few weeks, you’ll have a better understanding of your spending habits and saving potential.

If you’re thinking that this is a LOT to do all by yourself, don’t worry, we’ve got your back!

Our Financial Experts can guide you on topics like cash flow management along with building your portfolio. At Vittae, we start with understanding your wants and needs to personalize your financial growth.

Download the app today to unlock your financial freedom.